The Investment Club Playbook:

From First Meeting to Financial Growth

Announcements:

- The second Technical Analysis SIG meeting will be on Tuesday, July 21st followed by the Options SIG on the 25th. See the SIGs webpage for details on all SIG meetings.

- Following the chapter meeting, please join us and our speaker for lunch at the Cape Fear Seafood Company (Village District).

Presentation Summary:

Have you ever considered starting an investment club but felt unsure of where to begin? Or perhaps you’re a member of an existing club and want to enhance its success. In this comprehensive presentation, you’ll receive a detailed blueprint for launching and maintaining a thriving investment club grounded in BetterInvesting’s proven discipline principles of fundamental investing. Attendees will discover practical strategies to overcome the initial administrative challenges of forming a club, create engaging and informative monthly meetings, and leverage shared research to minimize individual biases.

What you will learn:

- Club Formation & Legalities: Learn how to overcome early administrative hurdles, draft robust club bylaws, and structure a general partnership.

- The Power of Pooling: Understand how shared research workloads and collaborative thinking can eliminate personal biases and build a top-performing diversified stock portfolio.

- Timeless Strategic Pillars: Discover how to implement BetterInvesting’s four fundamental investing principles within your club.

- Operational Excellence: Gain insights into the mechanics of running highly organized and productive meetings, and utilize specialized platforms to automate stock idea generation and analysis.

- Idea Generation Techniques: Explore strategies to keep your club pitches fresh and engaging through various industry stock studies and periodic collaborative “Stock Challenges.”

Meeting Details:

Date: Saturday, August 8th, 2026

Time: 10:00 a.m. ET (mix and mingle starts at 9:30)

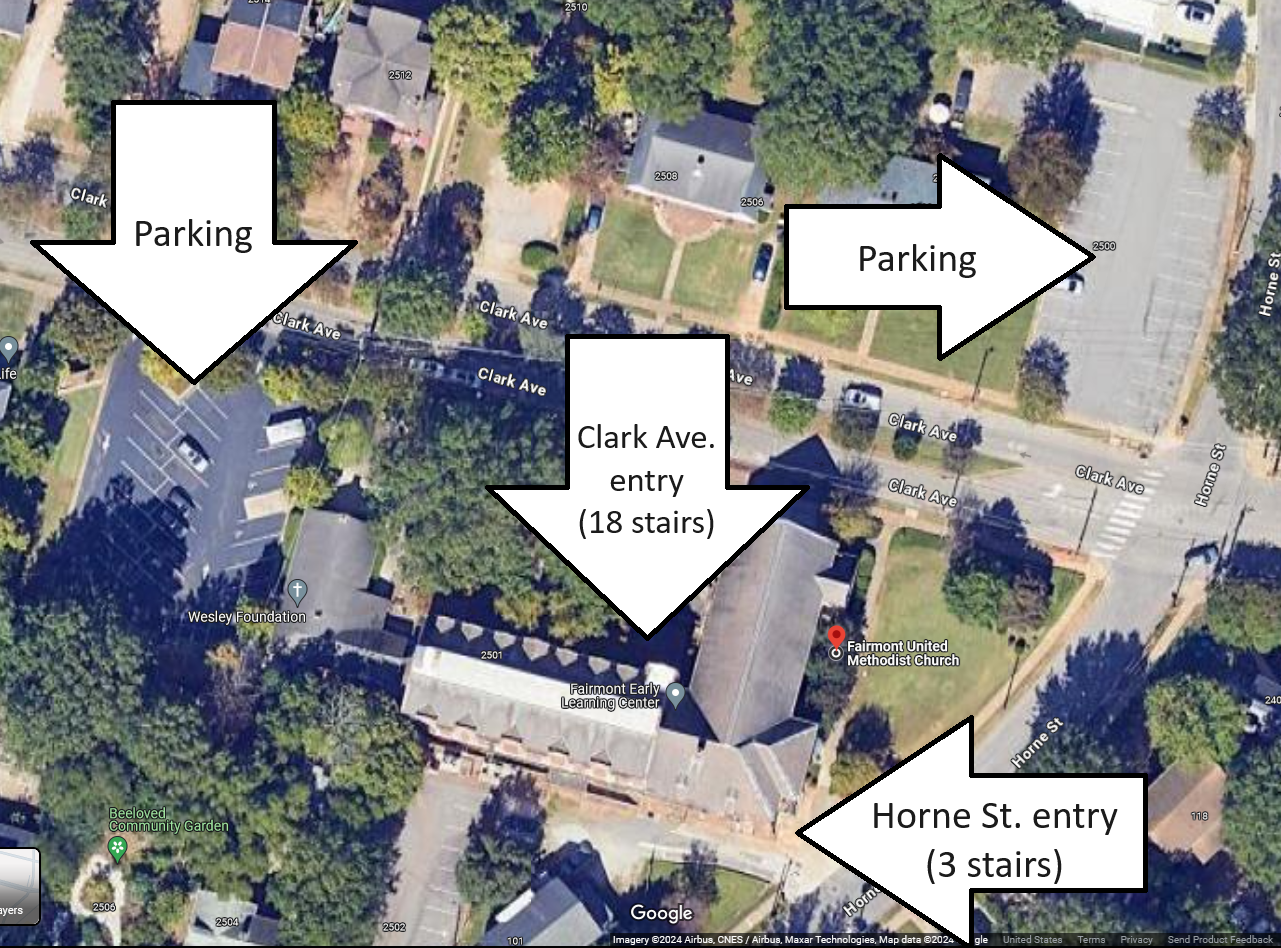

Location: Fairmont United Methodist Church: 2501 Clark Avenue Raleigh, NC 27607. See map of Fairmont for parking, building entrances, and the number of stairs entrances require.

{kind=link}

Virtual access: To register to attend the Zoom webinar, please purchase a ticket on our chapter’s Square account. Then, please register with Zoom so you can receive reminders one and 24 hours before the meeting.

Cost: $10 cash (in-person) or electronic payment (webinar); $5 for students (email president@aaiirtp.org for webinar access); first time in-person attendee: free

Before attending in person, please read: the AAII Protocol for In-Person Meetings

If you feel sick, please join us virtually.

About Our Speaker

Keith Felton, Ph.D., a retired Mechanical Engineer, embarked on a journey to learn about investing in the stock market in his early 20s. Inspired by the benefits of investment clubs, he, along with his wife and a small group of friends, founded a club based on the principles of BetterInvesting (BI). Keith served as the club’s president for 35 years, during which time the club built its investing knowledge and portfolio. Drawing from the principles of BI, Keith developed his own portfolio and personal wealth-building strategy. Currently, he serves as a director for the North Carolina Chapter of BI and is the President of BI, North Carolina (NC) Chapter’s model investment club, known as the NC Triad Model Investment Club.